-

Small business lending has undergone a dramatic digital transformation with digital platforms, embedded finance ecosystems, and automated credit underwriting. However, the rapid digital transformation has also increased exposure to sophisticated fraud schemes. The rise of generative AI has lately amplified these risks even further. AI-generated documents, synthetic identities, and deepfake-enabled verification bypasses are increasing rapidly…

-

Organizations are allocating substantial resources towards AI/ML, advanced analytics, and automation to fuel growth and strengthen their competitive advantage. However, despite significant investments, many of these initiatives stall or underdeliver. Why? A fundamental yet often overlooked reason is the absence of robust data hygiene practices. Just storing data isn’t enough, it needs to be clean,…

-

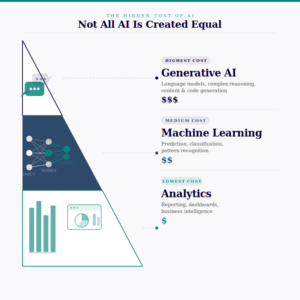

Artificial Intelligence is transforming how businesses operate but one critical aspect is often overlooked: AI pricing and cost control. Many organizations rush into AI implementation without understanding how AI pricing works, especially token-based pricing models used by large language models (LLMs). The result? Unpredictable costs. Budget overruns. Poor ROI. How AI Pricing Works: Understanding Token-Based…